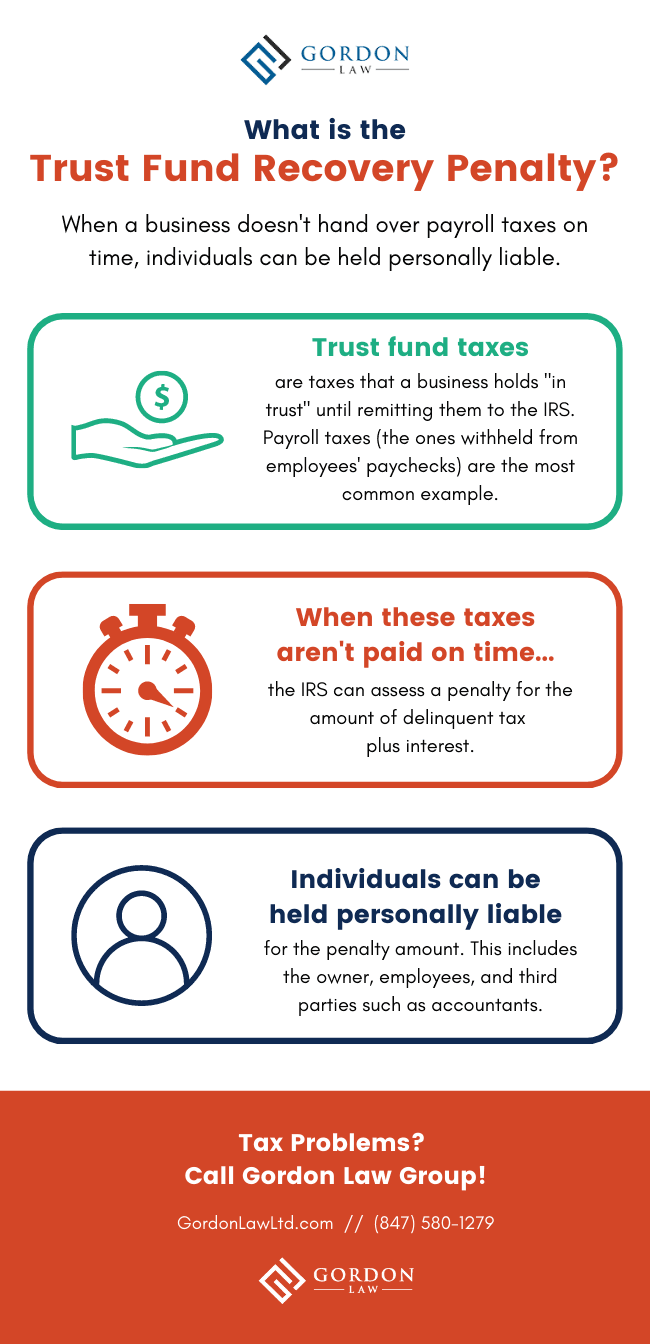

The Trust Fund Recovery Penalty (TFRP) allows the IRS or a state tax board* to hold individuals personally liable for certain taxes that were not paid to the government on time. In the eyes of the Tax Man, this is akin to theft, and the penalties can be severe.

The most common types of taxes involved in a TFRP are employment taxes and sales taxes.

During an investigation, the taxing authority must establish that trust fund taxes were willfully unpaid, and also determine who is responsible for the error. The individuals deemed responsible can be on the hook for the full amount of unpaid tax, plus interest, but there are ways to fight the TFRP or mitigate the situation.

Read on to learn what trust fund taxes are, how the Trust Fund Recovery Penalty is assessed, and how to fight it.

*This penalty may go by a different name at the state level, depending on your state. For example, Illinois has the 100% Personal Liability Penalty, which works similarly to the TFRP. For simplicity’s sake, we will use the term Trust Fund Recovery Penalty throughout this article.

What are trust fund taxes?

You may be thinking of the trust funds held by wealthy families, but in this case, trust fund taxes refer to the taxes that businesses must withhold from employees or customers and remit to the state.

Employment taxes:

Businesses are responsible for withholding certain taxes from employees’ paychecks, including income tax, Social Security, Medicare, and unemployment tax. As a business owner, you hold these taxes “in trust” for your employees, then hand them over to the IRS and/or state tax board later.

Sales taxes:

When you sell items that are subject to sales taxes, you must collect sales tax from your customers. You hold these funds in trust until you remit sales and use tax to the state tax board.

Note: Sales and use taxes are under state jurisdiction, so any penalties for failure to pay these taxes on time would be assessed at the state level.

How much is the Trust Fund Recovery Penalty?

The IRS Trust Fund Recovery Penalty is equal to the amount of trust fund taxes that were withheld and not paid. Interest will also accrue starting on the date the tax was due.

Although the TFRP only applies to taxes that were actually held in trust (i.e. the payroll taxes withheld from employees’ paychecks or the sales taxes collected from customers), other penalties can apply if these taxes were never withheld/collected to begin with.

Who is responsible for unpaid payroll taxes or unpaid sales tax?

Anyone at the company who is found to be both responsible and willful can receive the Trust Fund Recovery Penalty. Both requirements must be met in order for the TFRP to be assessed.

Responsibility

Any individual who is responsible for collecting and paying trust fund taxes could be eligible for a Trust Fund Recovery Penalty assessment. In a small company, the owner of the company is typically considered responsible by default. However, it doesn’t stop there. Who’s running payroll? Who manages the books? Who signs the company’s checks?

Employees, bookkeepers, accountants, and third-party administrators are all fair game when it comes to the TFRP. A key factor of the responsibility test is whether the individual has the power to decide which bills are paid.

Willfulness

In addition to being responsible, an individual must be deemed willful in their nonpayment before they can receive an IRS Trust Fund Recovery Penalty. Choosing to pay other bills while failing to remit trust fund taxes, for example, may be considered willful behavior. Reckless disregard for the duty of collecting and paying these trust fund taxes can also establish willfulness.

It is not necessary to have bad intent. For example, the owner of a company may choose to cover payroll rather than taxes, thinking that the taxes will be paid at a later time. However noble the intention is, paying other creditors over the IRS or state taxing authority may be seen as willful conduct.

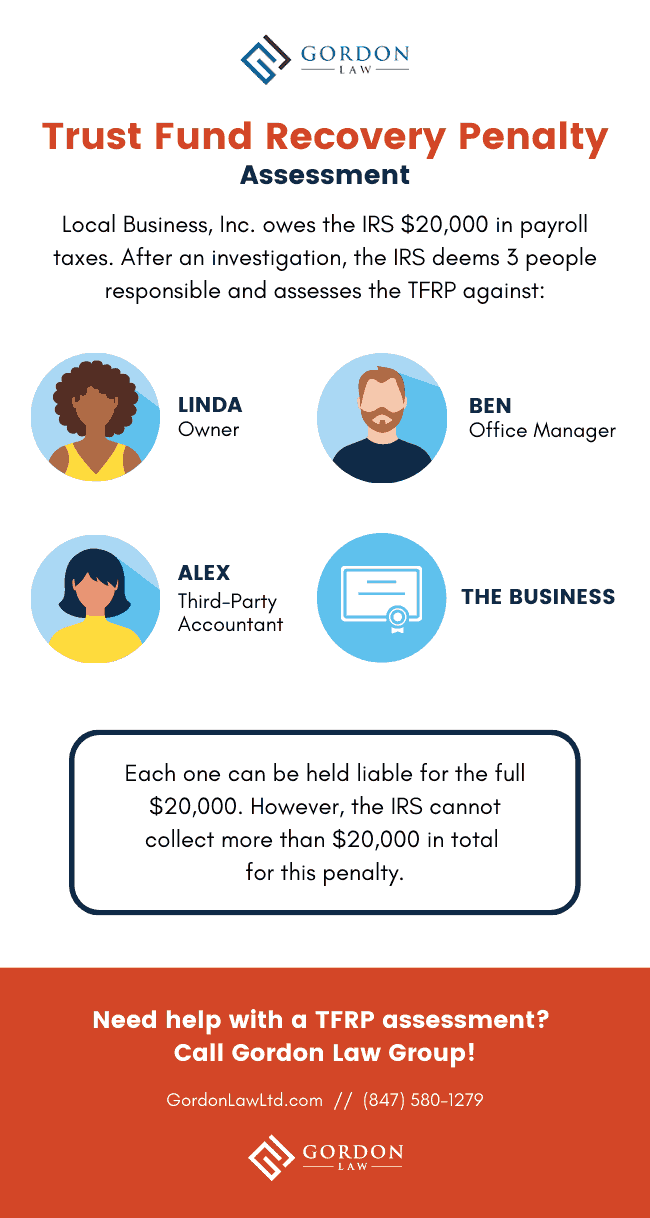

The TFRP can be assessed against multiple people at once

An individual, or multiple individuals, can be liable for a Trust Fund Recovery Penalty, and the IRS or state tax board can enforce collections from any or all of them.

Let’s look at an example of what can happen if multiple people receive the penalty assessment:

Local Business, Inc. owes the IRS $20,000 in payroll taxes. After an investigation, the IRS deems 3 people responsible: Linda, the owner; Ben, the office manager; and Alex, a third-party accountant.

Linda, Ben, Alex, and the company are each liable for the full amount. Any one of them could have to fork over the $20,000 in full. However, the IRS cannot collect more than $20,000 total for this case.

How the Trust Fund Recovery Penalty investigation works

To assess the Trust Fund Recovery Penalty, the IRS must first send a notice of an investigation, either by mail or in person. Then, a revenue officer will request company documents in order to narrow down a list of suspects.

The revenue officer will schedule interviews with any individuals who could be considered responsible. If an individual refuses the interview, they could receive a legal summons and be forced to comply.

In an IRS case, the revenue officer will complete IRS Form 4180: Report of Interview with Individual Relative to Trust Fund Recovery Penalty or Personal Liability for Excise Taxes. This document is essential to the investigation, as it helps establish both responsibility and willfulness—the two requirements of a TFRP assessment.

If you’ve been selected for a Trust Fund Recovery Penalty interview, it’s wise to hire an experienced tax attorney to represent you.

After all of these interviews are complete, the revenue officer will decide who receives notices of potential liability for the Trust Fund Recovery Penalty.

Note: The process may be different for your state’s equivalent of the TFRP; in Illinois, no investigation is required for the penalty to be assessed.

Challenging a TFRP assessment

Individuals who are deemed to be responsible and willful will receive Letter 1153(DO) and Form 2751: Proposed Assessment of Trust Fund Recovery Penalty.

It is possible to file a written protest to the proposed assessment within 60 days. The protest should be prepared by a professional advisor, such as a tax attorney; it must have as much documentation as possible to support a lack of responsibility or lack of willfulness.

Trust Fund Recovery Penalty payment

Once all avenues of tax appeal are exhausted (or skipped), the IRS will officially assess the penalty and send a bill to each individual who is considered liable. There is still a chance to fight the TFRP at this stage through formal or informal claims.

The individual can either request an abatement of the penalty, or make payments and sue for a refund in court. Payment plans can also be arranged to make any resulting tax debt more manageable.

If you’re dealing with the Trust Fund Recovery Penalty, don’t try to fight the IRS on your own. We’re here to help you navigate the IRS maze; give our tax attorneys a call at (847) 580-1279 or contact us online to discuss your options!